Starting a retail business in the UK: understanding your year-one costs

In this article, we explore the main expenses to consider before opening a retail store, ways to reduce them and how to use business finance to fund your year-one costs.

Starting a retail business in the UK doesn’t have to be expensive. Depending on your business plan, you can even start a business with no money. But for most entrepreneurs, you’ll need some initial investment to get your started. The first step is to understand the upfront costs involved and what financial support you may need.

What are the main expenses involved in starting a retail business?

Operating in retail involves certain expenses you may not see in other sectors – inventory, utilities, product liability insurance, shop rental costs, etc. Online retail companies and service-based business models typically have lower overheads, with costs often centred around technology and specialised equipment.

Consider the upfront investment required before opening your doors, such as securing a store location and kitting it out, stock and staffing needs, business rates and promotional activities for launch.

So, let’s look at the main expenses to expect when starting a retail business,

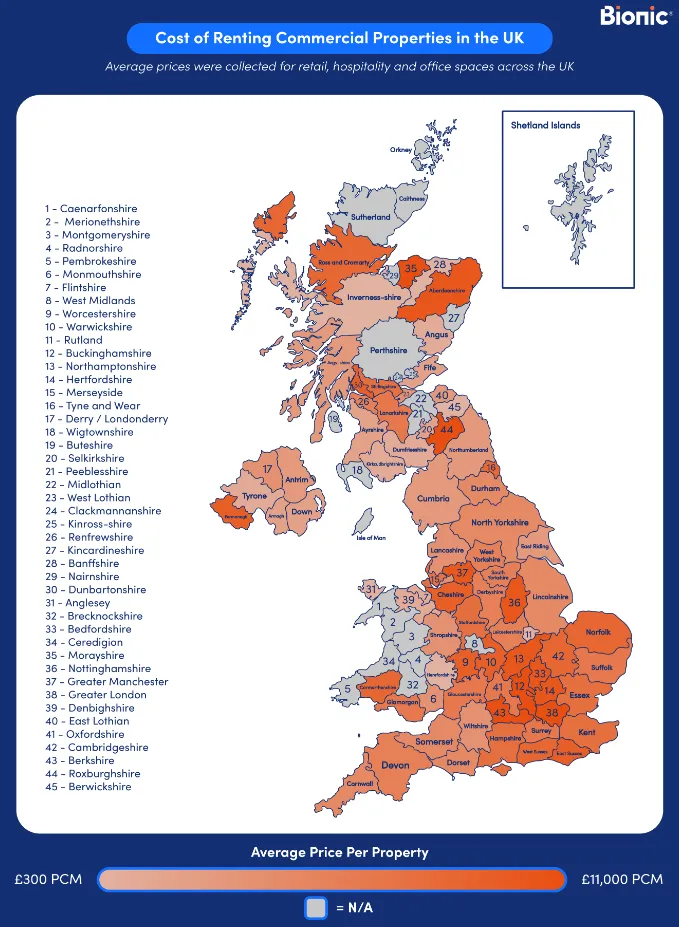

Rent and business rates

You’ll need to calculate potential business rates and rental prices. If you’re not wedded to a particular location, research different areas in the UK and see which have the most affordable rates.

Average rental costs in major UK cities

Unsurprisingly, South East England has the highest rental costs. London, Cambridge and Oxford are around £50 per square foot per year,* whilst most of the cheapest areas are in Wales, Scotland and Northern England, including cities like Hartlepool, Rotherham and Blackpool (between £12-15 per square foot per year).*

To secure affordable locations, explore up-and-coming locations and look at market trends and successful areas in the UK for your retail business. Plus, negotiating leases can help reduce upfront costs.

Understanding and calculating your business rates

Also, there are business rates to consider. These are taxes charged on most non-domestic properties, including shops, pubs, offices and warehouses, based on the property's rateable value. For small businesses, they’re typically around 50% of the value. See the HMRC’s dedicated page for estimating your business rates.

The good news? You may be eligible for the government’s Retail, Hospitality and Leisure Business Rates Relief Scheme, which eases the burden.

Stock and inventory

Judging initial inventory investment is difficult, as you don’t have revenue and sales stats to back you up, but keeping a healthy inventory with minimal waste is vital for retail business success.

The importance of good stock control and inventory management

Research your market thoroughly, accounting for your marketing spend, to estimate likely demand and predict stock levels you’ll need from the outset.

Use smart data systems to analyse and predict inventory requirements to avoid costly excess or empty shelves, which impact your reputation and hit you in the pocket.

{{retail-blog-cta="/seo-components"}}

Cost-Saving strategies for managing inventory effectively

Here are a few tips for efficient inventory management:

Retail demand planning helps you predict how much stock you need to meet customer demand. This starts with building a strategic framework and using forecasting tools and techniques to balance supply and demand.

Use inventory management systems to run a tight ship – monitoring stock control reduces wastage and prevents stockouts.

Get to know your customers – audience research and consumer insights will help you set appropriate pricing and meet expectations.

Explore financial solutions, such as inventory finance – this can help you ease cash flow, invest in inventory during peak seasons and cover unexpected costs.

Retail business insurance costs

When starting a retail business, you need to cover yourself against various risks and potential claims. So, get to grips with your likely retail business insurance costs.

Here are the key types of insurance retailers need:

Public liability: Protecting you against claims from members of the public for accidents, injuries or property damage on your premises. The average cost is £120 per year but costs depend on size, location and cover level (£1-5 million).

Product liability: Covers claims related to injury or damage caused by your products. Premiums vary widely, depending on product types and risk factors, but expect to pay between £50 and £500 per year.

Cyber insurance: Relating to risks arising from data handling, payment processing, etc. It covers data breaches, cyberattacks, potential legal fees or IT system downtime. Premiums range from £100 to £500 per year for small businesses.

Employers' liability: Covering businesses against claims from staff who get injured/ill when working. Premiums depend on how many employees you have, but typical costs range from £60 to £300 per employee annually.

Buildings and contents insurance: Relating to damage to your store or the contents inside. Again, premiums vary, based on your store’s location and contents value, but quotes start from around £100 per year.

Stock cover: Insuring you against inventory theft or damage, including break-ins, flooding and fires. Insurance costs are approximately 0.5% to 1% of total stock value.

Business interruption insurance: Covering you in the event of being unable to operate due to unforeseen events (fire, floods, energy/communications failure, etc). Some providers have a minimum premium, and costs are generally 0.1% to 0.3% of annual turnover.

Utilities and services

Rising energy costs are a concern for small businesses in the UK. While recent economic volatility has eased a little, utility prices are still a big issue for SMEs.

As a retailer, carefully budget for things like electricity, water and internet connectivity. Also, explore energy-saving measures like energy-efficient lighting and equipment, building insulation, going paperless and carrying out regular audits to minimise utility expenses. Get insights from comparison websites and money-saving experts to find the best value.

Marketing and promotions

A successful retail business doesn’t grow silently. Most digital agencies recommend new businesses allocate between 10-20% of initial gross revenue to marketing activities. So, set aside enough marketing budget to build your brand and reach your audience effectively.

Although paid search and social channels and remarketing ads help generate revenue, you should explore cost-effective marketing tactics alongside your advertising spend. Here are a few options to consider:

Try free/affordable research and analytics tools to learn about consumer trends and customer preferences

Grow your retail brand on relevant social networks, with regular posting and varied content to engage your audience and community

Leverage localised SEO and regional advertising

Collaborate with local businesses and forge beneficial partnerships

Build anticipation ahead of launching and opening your retail store

Combining organic and paid marketing tactics across channels can help you keep costs down while achieving great results.

{{benchmarkingtool-cta="/seo-components"}}

How to reduce costs when starting a retail business

The investment required to start a new business can be daunting. Want to know how to cut costs in your retail business? We’ve outlined ways to reduce business costs and ease pressure.

Negotiating better rates and terms

Securing the best rates and terms is an important money-saving measure, so negotiate with your suppliers, service providers and landlords. This may sound easier said than done, so here are a few tips for negotiating better deals:

Explore longer-term commitments to lower monthly costs – many insurers and software providers offer discounts for paying annually, while bulk purchases reduce inventory costs.

Build good relationships and open communications with providers – this can lead to favourable terms or leeway in the future.

Do your research – understanding market rates and average service costs strengthens your negotiating position.

Demonstrate your value – showing reliability and flexibility builds trust, which helps you secure cheaper rates and better payment/delivery schedules.

Leveraging government support and relief schemes

The UK government has various support for small businesses, including grants and the Retail, Hospitality and Leisure Business Rates Relief Scheme. This scheme offers relief to businesses using properties as shops, restaurants, cinemas, music venues, and other hospitality purposes. Those eligible can enjoy up to 75% relief on their business rates – capped at £110,000 per business.

You could also secure a government grant, receiving reduced business costs, free equipment and cash awards. Funding bodies consider business size, location, sector and purpose.

Once you’ve fully considered the major expenses of starting a retail business you may need additional capital. Business finance can help you lay the foundations, fuel initial growth and ease the burden of year-one costs.

There are various options available to retailers, such as:

Many retailers use revenue-based finance to access a lump sum and make repayments as a percentage of future card sales, so payments adjust as you grow.

Introducing iwoca

Iwoca offers a range of flexible business finance solutions to help retailers fund initial costs, from securing store locations to investing in stock, systems and promotions. Our business loans offer fast access to capital, which can be invested where it’s needed to kick-start your retail business.

You can be approved within 24 hours and enjoy flexible terms and affordable monthly repayments. It’s easy to apply for a business loan with iwoca. So explore our finance solutions to see how we can get you off to a flyer.

Rowland is an experienced B2B content writer specialising in fintech and financial services, primarily covering financial trends and solutions for SMEs and growing businesses.

About iwoca

iwoca is one of Europe's leading non-bank lenders. Since 2012, we've lent over £4.5 billion to 100,000 small and medium-sized businesses in the UK and Germany.

iwoca has won a number of awards, including Moneynet's best small business lender (2024) and best small business provider (2025). We've also been featured in major media outlets including The Independent, Forbes and the Financial Times.